Experience Modification Calculator

Estimate experience modification factors and compare results between the current and updated plans.

By maintaining a transparent and consistently applied Experience Rating Plan, PCRB helps ensure:

This structured approach reinforces confidence in Pennsylvania’s workers’ compensation system and supports long-term market stability.

PCRB updated the Pennsylvania Experience Rating Plan effective April 1, 2024. These changes were intended to preserve actuarial integrity, enhance clarity, and ensure the plan continues to function as a reliable and equitable pricing tool for all qualifying risks.

Members should review resources available on this page to understand what is changing, how the updates affect experience modifications, and what actions—if any—may be needed.

Estimate experience modification factors and compare results between the current and updated plans.

Plain-language overview of Experience Rating principles and the 2024 plan updates

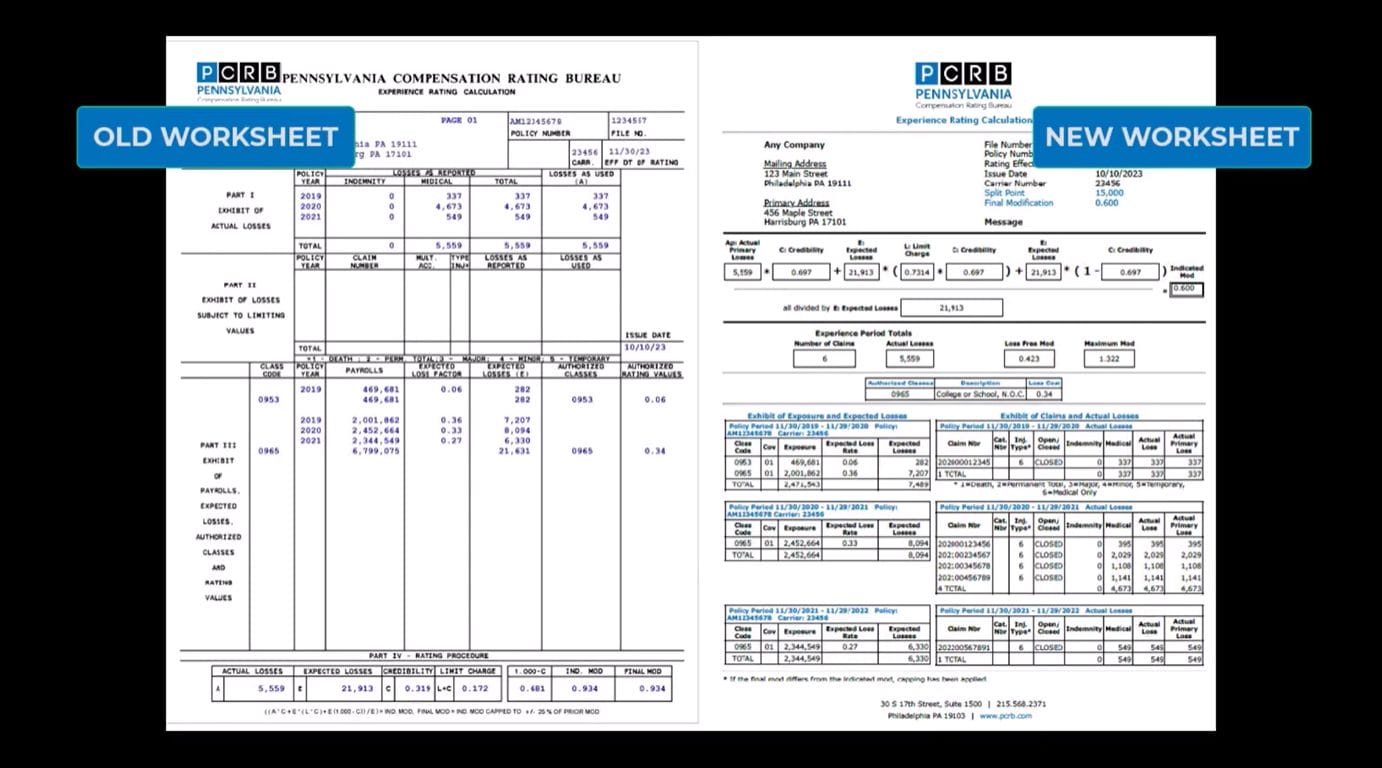

Plan comparisons, key terminology, and glossary supporting interpretation of the 2024 mod worksheet.